Reference Number

A228302

描述

Across India's smaller cities, towns, and semi-urban stretches, a quiet economic shift is underway. Thousands of people — daily wage workers, auto drivers, small vendors — are stepping into self-employment through one practical decision: buying an electric rickshaw on a loan.

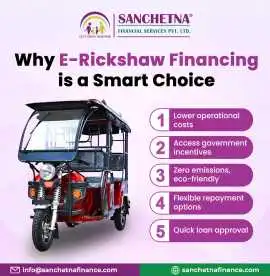

It is not a complicated story. An e-rickshaw costs between ₹1 lakh and ₹1.6 lakh. A driver who owns one instead of renting can earn ₹600 to ₹1,500 per day. The math works — and with the right e-rickshaw finance, the entry barrier is lower than most people expect.

Why traditional loans kept most drivers out

Until recently, financing an electric rickshaw through a bank was nearly impossible for most buyers. Banks required collateral of up to 1.5 times the loan amount — an asset that a daily-wage earner simply does not have. Credit scores were evaluated on formal income history, which excluded most first-generation entrepreneurs entirely.

The result was predictable. More than 50% of e-rickshaw drivers in India operated on a daily rental model, paying ₹200 to ₹400 per day to a fleet owner just to use a vehicle they would never own. Earning, but never building.

NBFC-based e-rickshaw loans changed this equation. No collateral required. No lengthy income proof. Just basic KYC documents — Aadhaar and PAN — and a verifiable intent to operate the vehicle commercially. Approvals in 24 to 48 hours. Disbursal on the same day.

How modern e-rickshaw finance actually works

Most NBFCs offering electric rickshaw loans today cover up to 80% of the on-road price. The borrower arranges a modest down payment, submits their KYC and bank documents, and can be on the road within a day or two of applying.

It is not a complicated story. An e-rickshaw costs between ₹1 lakh and ₹1.6 lakh. A driver who owns one instead of renting can earn ₹600 to ₹1,500 per day. The math works — and with the right e-rickshaw finance, the entry barrier is lower than most people expect.

Why traditional loans kept most drivers out

Until recently, financing an electric rickshaw through a bank was nearly impossible for most buyers. Banks required collateral of up to 1.5 times the loan amount — an asset that a daily-wage earner simply does not have. Credit scores were evaluated on formal income history, which excluded most first-generation entrepreneurs entirely.

The result was predictable. More than 50% of e-rickshaw drivers in India operated on a daily rental model, paying ₹200 to ₹400 per day to a fleet owner just to use a vehicle they would never own. Earning, but never building.

NBFC-based e-rickshaw loans changed this equation. No collateral required. No lengthy income proof. Just basic KYC documents — Aadhaar and PAN — and a verifiable intent to operate the vehicle commercially. Approvals in 24 to 48 hours. Disbursal on the same day.

How modern e-rickshaw finance actually works

Most NBFCs offering electric rickshaw loans today cover up to 80% of the on-road price. The borrower arranges a modest down payment, submits their KYC and bank documents, and can be on the road within a day or two of applying.

国家

India

州/地区/省

Uttar Pradesh

城市

Lucknow

邮政编码

226017

地址

B-348/3, Rajajipuram, Lucknow - 226017 (U.P.)

- 2 观点

-

查看二维码

- Report Listing Cancel Report

-

- Current rating: 0

- Total votes: 0